{kind=link}

S Marshall, CC BY 3.0, via Wikimedia Commons

The shape of Trussonomics is becoming clearer. Assuming she survives in office, which given how unpopular she already is with her own MPs might be an optimistic forecast, what is the future going to hold, and what might it mean for the 99 per cent of use who aren’t bankers? Richard Murphy explains.

Unless you work for a far-right think tank there is now near universal agreement that Kwasi Kwarteng presented the all-time worst budget in living memory last week, and maybe way beyond that.

Let’s forget the details (except all those tax rises for the rich and bigger bonuses for bankers) and summarise what he got wrong from the macroeconomic (big issue) perspective.

What he said was that he would run the already forecast deficit for the next year, of about £75 billion. Then he said he would spend £60 billion every six months to support households and businesses with the energy crisis, without explaining where the numbers came from.

On top of that, he said that they would give tax cuts of at least £45 billion which will add to the deficit in the next year.

And we should remember that the day before he spoke, the Bank of England had also said that it wants to sell £80 billion of the government bonds that it holds back to the financial markets in the next year.

In all then, Kwarteng and the Bank (who, whatever they might say, seemed not to talk to each other about these plans) want more than £300 billion from financial markets in the next year.

To compound this, the Bank did not say where interest rates were going, whilst Kwarteng merrily suggested balancing government budgets no longer matters when for the last twelve years his own party has said that is all economics is about.

Bizarrely, both Kwarteng and his party were wrong. That is because the relationships between money creation, spending, what the government calls debt and QE (quantitative easing) is a complicated one that it’s very clear neither understand.

But what you can’t do is tell markets not to worry when you are planning to ask them for vastly more money in the next year than any other government in history when your predecessors have all said it would be a disaster to do such a thing.

Kwarteng was like the new school teacher who tells their pupils running across roads without looking is just fine when every previous teacher disagreed. Of course the parents would be spooked. And so were markets. Confusion reigned.

Markets don’t like confusion (unless you’re a hedge fund manager, when you love it) and so the mainstream market decided to dump everything to do with the UK, whether it was sterling deposits or government bonds, as fast as they could.

Rationally, no one could blame them for doing that. When it looks like someone incompetent is in charge why trust your finances to them? And, Kwarteng looks to be the most incompetent Chancellor the Tories have ever found, and they have got a lot of challengers for the title.

So, where are we now? First, the pound has collapsed, and the only reason was Kwarteng. Sure, the dollar is overvalued, but it is against all currencies, and the pound has fallen against everything else as well, so this is a particular UK problem with only one explanation.

In response, Liz Truss apparently wanted to say nothing at all. That is fine if you are a dictator who does not care about the consequences of your actions. Kwarteng was eventually allowed to say something. It was that he will have an announcement to make in eight weeks’ time.

As reassurance to febrile markets goes, that was worse than useless and only reinforced the lack of trust traders around the world already felt in a man so clearly out of his depth. But what it did do was turn the whole focus onto the Bank of England.

We now know from the Governor and Chief Economist of the Bank that it will take whatever steps are necessary to control inflation (bar sacking Truss and rejoining the EU, both of which are needed but which they can’t deliver). What they mean is that we will get interest rate rises.

These will also not happen before November, but, unlike Kwarteng, the markets still trust the Bank, so for now they have assumed that these rate rises will happen, and are happy.

How big will those increases be? Markets are pricing base rates at around 6 per cent now. At present they are 2.25 per cent. So, at a minimum the rate increase in November is 2 per cent, and it is likely to then go up again at following meetings by maybe 1 per cent a time until the 6 per cent rate is hit early in 2023.

What’s the impact? The pound may fall no further. Even so, the fall we’ve seen might wipe out many of the gains on inflation that the energy price cap was meant to protect us from.

A fall in the value of the pound impacts everything we buy from abroad. That includes gas, petrol and more than half our food. It also includes all that manufactured stuff we get from China and a lot of raw materials. Inflation is bound to rise, even if the pound holds now.

Kwarteng has in that case destroyed attempts to keep inflation under control.

But worse, increasing interest rates feeds through to higher mortgage rates. If base rates rise by 6 per cent or thereabouts in a year so do mortgage rates, and very few families in the UK will be able to afford mortgages at 7.5 per cent or more that they are likely to be offered very soon.

Unambiguously we have a housing crisis coming, and no one is talking about it.

And let’s be clear, there is no obvious answer unless the government stops borrowing, which would reduce the pressure for increasing rates considerably.

There are two ways for the government to stop borrowing. One would be to slash public services. The other is quantitative easing. Let me address them in turn.

What we are hearing from the government and from the right-wing think tanks that clearly control it is that by November we will be told about the massive reforms to public services that they are planning. There are likely to be three elements to this.

One is straightforward cuts on the basis that it will be claimed that many services we have enjoyed for 75 years can no longer be afforded. That, of course, is not true. We could afford what we have always enjoyed, but 12 years of Tory government has destroyed these services.

Deliberate underfunding has now left these essential services so denuded of investment that the cost of restoring them is high, but not impossible, unless you really do not like state services. Truss and her gang hate state services. They have never disguised the fact.

So what I actually suspect will happen is that fees and charges will be introduced for many services. In that case charges to see GPs will happen. Expect schools to ask for payments for some lessons and supplies. Social care will be even harder to get.

And wherever possible there will be privatisation. So insurance-based health and social care systems will be proposed as a precursor to sale of state activities. The aim will be to reduce debt – and the current recklessness will be used as an excuse for the need for that.

The destruction of state services, from the NHS onwards, will be on the cards from November if Truss makes it that far. This crisis might have been created to make this a possibility. There is no mandate for this, but democracy will not worry Truss, although it might her MPs.

What is the alternative? The deficit the government now plans could be alternatively funded. QE is one option. But given the scale of the crisis even that seems unwise and instead the Bank of England should simply lend the government the money to fund the deficit, interest-free.

At the same time, it should limit the interest paid on deposits held by commercial banks with the Bank of England to contain interest costs to the government.

Legally this is possible. Post-Brexit the government has no obligation to sell bonds to fund its deficit. And there is now no legal constraint on the government borrowing from its own bank, which can very easily create all the money required.

Will that add to inflation? I doubt it, and in any event that inflation would be better than mass unemployment and homelessness which is the alternative if interest rates rise as far as markets expect. Inflation is better than devastation.

And will the pound fall? Maybe, but not a lot, I suspect, when markets appreciate that this stabilises an economy on the brink of collapse, which is what they expect right now.

And would we need spending cuts in that case? I can see no reason for them, is my fair response.

But will markets react adversely? They might. But for all the reasons noted, I doubt it. They will realise that this is the ultimate backstop choice that has to be taken now to avoid calamity.

I can’t see a lot else that is going to keep the economy from total collapse right now. I wish I could, but something this radical – and simple – is now required. Most things hang on it, in my opinion. Avoiding economic devastation is the task right now. This plan does that.

PS Apologies for the length. I don’t just write these threads to explain what I think: I write them to work out what I think. That takes a bit of effort sometimes, hence how long they are.

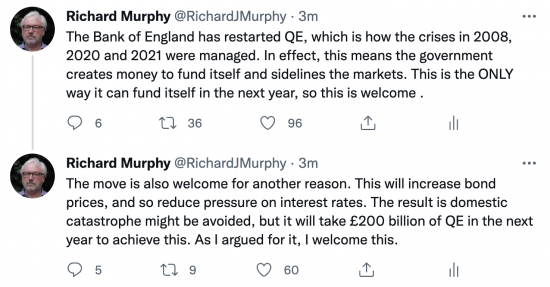

UPDATE:

I have just posted these tweets:

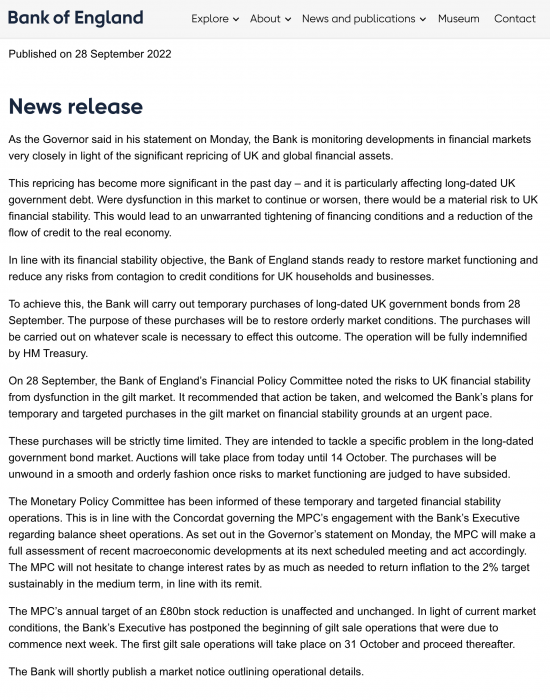

They are a response to this Bank of England announcement:

This policy is backed by the Treasury. It is the most staggering admission of failure by a new government of the UK, probably ever, coming as it does three weeks after it assumed power.

I suspect the interventions will be for much longer than the BoE suggests.

I also suspect, very strongly, that quantitative tightening (the Bank selling bonds) that is now scheduled for November now will not happen: they can’t buy bonds one month and sell them the next without adding to market confusion, although as yet they (as incoherently as Kwarteng in this regard) do not seem to have appreciated that.

This is a staggering shift in policy in such a short period of time. But as I said this morning, only government money creation can solve this problem now. I just think that the Bank has not realised how much is required.

You can read more from Richard on his blog.